Same-day financing allows small business owners to apply, receive approval, and access funds within 24 hours—sometimes within just a few hours of completing the application process.

Unlike traditional banks that may take weeks to approve a business loan, same day business loans focus on speed. When managing cash flow gaps, covering payroll, or responding to unexpected expenses, fast business funding can mean the difference between business growth and business disruption.

However, fast cash loans can come with higher costs, origination fees, and shorter repayment terms. Before borrowing, business owners should carefully evaluate the total cost of capital and understand how repayment will impact their business’s cash flow.

In this guide, we’ll explain how many business owners use same day business funding, outline available business financing options, and help you compare lenders responsibly to keep the business running.

What Are Same-Day Business Loans?

Same-day business loans are business funding options designed to provide capital within hours of approval. Most same day lenders operate online using automated underwriting and digital bank verification instead of the slower review processes used by traditional banks.

If approved in the morning and final contracts are signed by noon, funds may be transferred to the borrower’s business bank account that same afternoon.

How They Differ from Bank Loans

| Feature | Same-Day Lenders | Traditional Banks |

|---|---|---|

| Approval Speed | Same day approval or 24–48 hours | 2–6 weeks |

| Documentation | Bank statements + basic business info | Extensive paperwork + business plan |

| Credit Requirements | Flexible credit score | Higher credit score required |

| Loan Size | Small to mid-range | Larger loans |

| Cost | Higher total cost of capital | Lower rates |

Important Distinction: Business vs. Consumer Same-Day Loans

It’s critical to separate same day business loans from high-risk consumer products like:

- Payday loans (often capped at $500, repaid by next paycheck)

- Title loans (require signing over your vehicle title as collateral)

- High-cost installment loans

Payday and title lenders frequently charge fees that can result in APRs of 400% or more. Title loans allow the lender to seize and sell your vehicle if you default.

These are consumer debt products—not business financing solutions—and can create severe financial harm.

Business owners should avoid using personal payday or title loans to fund business operations.

Funding Timelines & Cutoffs

Most same day business funding depends on:

- Submitting the application early in the business day

- Connecting your business bank account instantly

- Accepting the offer before lender cutoff times (often 2–4 PM local time)

Delays in document submission can push funding to the next business day.

How Same-Day Business Loans Work

1. Online Application Process (5–15 Minutes)

Most lenders allow businesses to complete applications digitally in 5 to 15 minutes.

You’ll provide:

- Business name and industry

- Monthly revenue

- Time in business

- Ownership information

- Social Security Number (for soft personal credit review)

2. Automated Underwriting

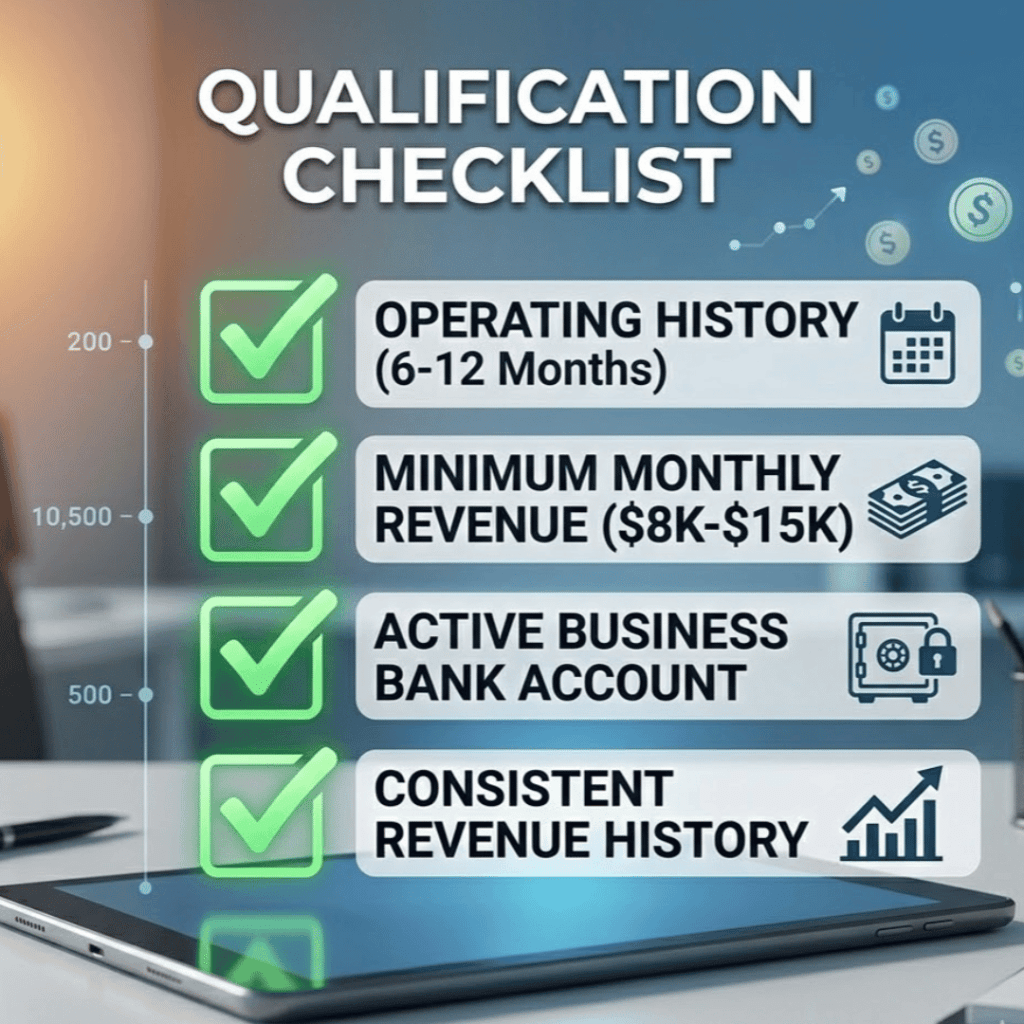

Online lenders evaluate:

- Revenue history

- Business bank statements

- Cash flow consistency

- Operating history

- Business performance

- Personal credit score (varies by lender)

Most same-day lenders require at least six months to one year in business.

3. Typical Document Requests

Prepare:

- 3–6 months of business bank statements

- Government issued ID

- Voided business check

- Secure business bank account login for verification

4. Offer Review & Acceptance

After approval:

- Review total repayment amount

- Confirm repayment schedule

- Check for origination fees or hidden fees

- Sign electronically

Funds are typically sent via ACH or wire transfer.

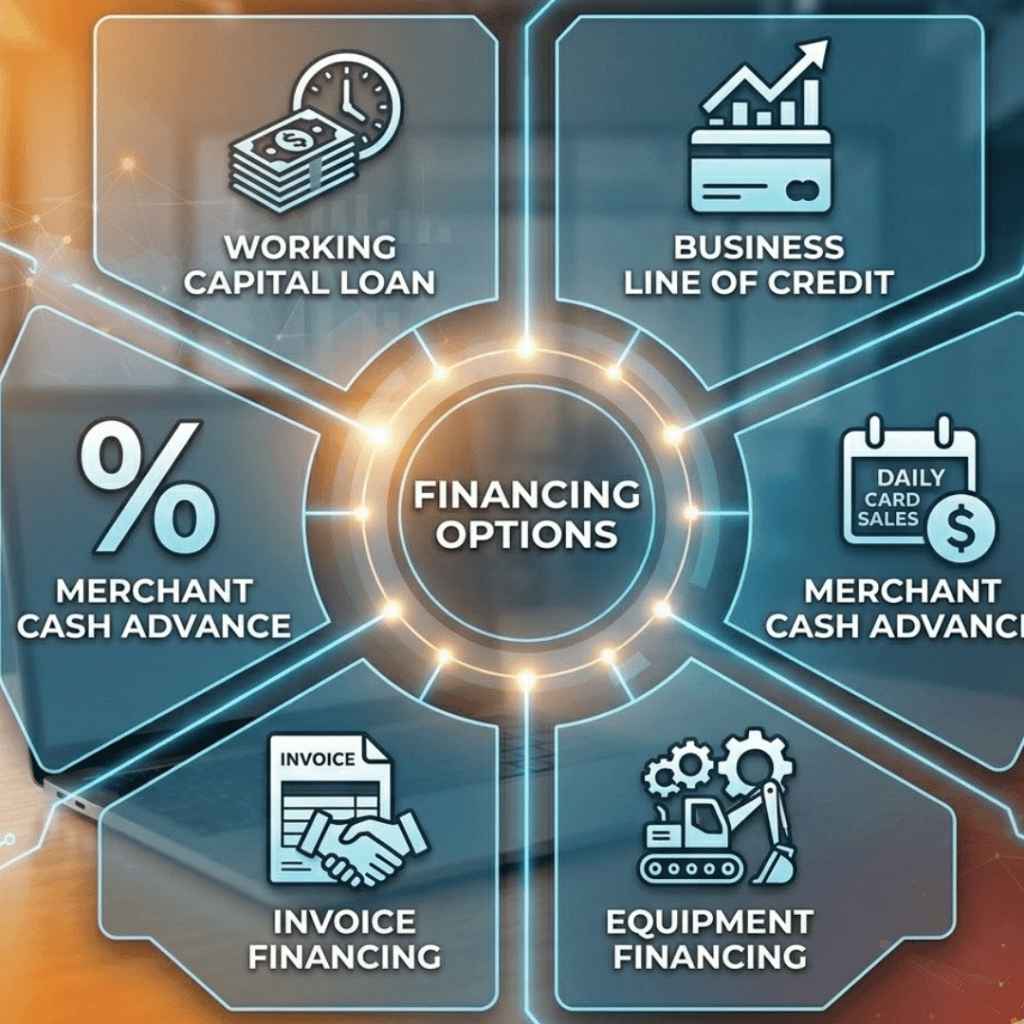

Types of Same-Day Business Loan Options

Working Capital Loans

Short term loans used to cover day-to-day expenses like payroll and rent.

- Lump sum funding

- Fixed payments

- Short repayment periods (3–18 months)

Be aware: Short repayment timelines can strain business cash flow if revenue fluctuates.

Business Line of Credit

A revolving credit structure that allows businesses to draw funds as needed.

- Credit limit established upfront

- Pay interest only on funds drawn

- Ideal for managing cash flow gaps

Once approved, accessing funds can be nearly immediate.

Merchant Cash Advance (MCA)

Provides a lump sum in exchange for a percentage of daily card sales.

- Uses factor rates (not traditional interest rates)

- Daily or weekly automatic deductions

- Repayment tied to revenue

⚠ Because payments are frequent, MCAs can pressure business cash flow.

MCA Repayment Example

If a business receives $50,000 with a 1.3 factor rate:

Total repayment =

50,000 × 1.3 = 65,000

That means the total cost of capital is $15,000.

If daily deductions are $650, repayment would take approximately 100 business days.

Factor rates do not translate directly into APR. Business owners must calculate total repayment — not just advertised rates — when comparing offers.

Invoice Financing

Advance funds against unpaid invoices.

Best for:

- B2B companies

- Established businesses

- Companies with strong accounts receivable

Funds are often available within 24 hours of invoice verification.

Equipment Financing

Used to purchase business assets.

- Secured by equipment

- Often lower rates than unsecured loans

- Fixed payments

Revenue-Based Financing

Repayments fluctuate based on monthly revenue.

Ideal for seasonal businesses or companies with uneven cash flow.

Recent Comments