Recent Comments

| Rahul Gupta on Business Loan with Bank Statem… | |

| Joe on How Cannabis MCA Funding Can H… | |

| John on Opening a dispensary? See how… | |

| Toluwalope Oyeleye on Advantages and Disadvantages o… | |

| Knote on The Ultimate Guide to Short Te… |

Bridges cash flow gaps, accommodating temporary revenue dips.

Fixed payments, longer terms, providing budgeting certainty.

Unlocks flexible funds, only pay interest on the amount you draw.

| Rahul Gupta on Business Loan with Bank Statem… | |

| Joe on How Cannabis MCA Funding Can H… | |

| John on Opening a dispensary? See how… | |

| Toluwalope Oyeleye on Advantages and Disadvantages o… | |

| Knote on The Ultimate Guide to Short Te… |

One Comment

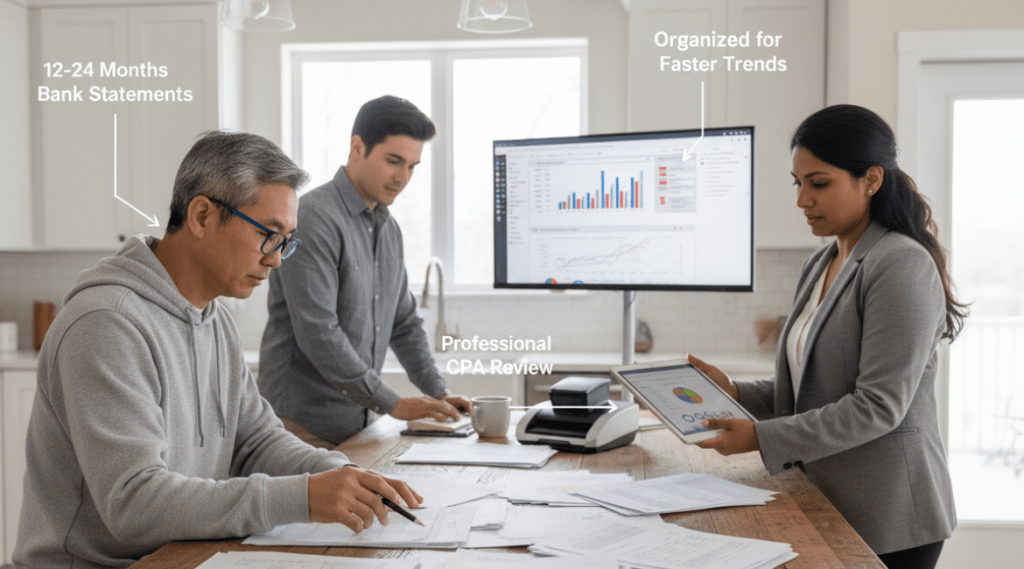

In this blog, the overview of business-loans based on bank statements simplifies the borrowing process a helpful option for small businesses with irregular income flows.