Setting up a business involves many crucial decisions, and perhaps none is more impactful than choosing your business structure. This choice influences everything from your day-to-day operations and personal liability to how much you pay in tax and your ability to raise money.

Another common option is the sole proprietorship, a simple and informal business structure that gives the owner complete control over decisions and operations, but does not provide the liability protection offered by LLCs and S Corps.

Understanding the fundamental differences between an llc vs s corp is essential for making an informed choice that aligns with your business goals. While they share some characteristics, particularly regarding liability protection, they have distinct operational and tax implications that can significantly affect your company’s trajectory. Unlike corporations, sole proprietorships and LLCs cannot sell stock to raise money, which is an important consideration for businesses seeking outside investment.

Starting with the Basics: LLCs and Asset Protection

Limited Liability and Simplicity

The Limited Liability Company, or LLC, is a highly popular choice for small businesses due to its inherent simplicity, flexibility, and minimal paperwork. LLCs are typically operated by their members, who manage the daily business activities and decision-making. The defining characteristic of an LLC is that it provides its owners, known as members, with robust personal liability protection. This crucial benefit means your personal assets—such as your home or savings—are generally shielded from business debts and legal liabilities. This protection makes LLCs a good choice for medium- or higher-risk businesses where personal asset protection is a primary concern.

LLCs typically require minimal ongoing formalities, such as maintaining an Operating Agreement and completing annual state filings.

Step-by-Step Formation of a Limited Liability Company

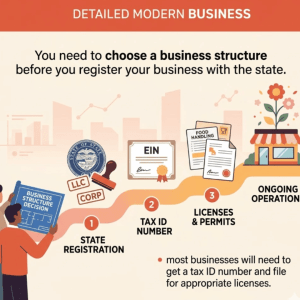

You need to choose a business structure before you register your business with the state. This critical decision forms the foundation of your future operations. Before registering, it’s important to create a business plan that outlines your goals, funding needs, and strategy for growth. Once the decision is made, the actual formation of an LLC is a relatively streamlined operational process. You must first prepare and file the appropriate state forms with your specific states‘ regulatory agency, which is most often the Secretary of State’s office.

Most businesses will also need to get a tax ID number (EIN) and file for the appropriate licenses and permits to operate legally within their industry and location. Consulting with business counselors, attorneys, and accountants can prove helpful when choosing a business structure and navigating these crucial early stages. Keep in mind that ownership rules, liability, taxes, and filing requirements for each business structure can vary by state, so local expertise is invaluable.

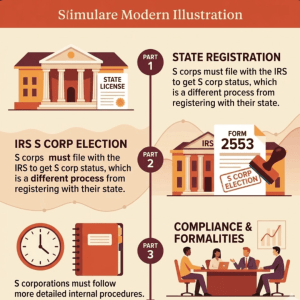

It is essential to understand that an LLC can have a limited life in many states. This feature might require dissolution and re-formation of the llc with new membership under certain conditions, such as when a member joins or leaves the company. This process is distinct from how a corporation operates. Many business owners plan to start as an LLC for simplicity and later elect S corp status using IRS Form 2553 when profits are high enough.

Ongoing Compliance for LLC vs S Corp and Management

Minimal Formalities and Flexible Management of an LLC

A major advantage of choosing an LLC is preferable for low administrative costs and flexibility while starting out. LLCs typically require minimal ongoing formalities compared to corporations. This difference is visually and operationally distinct. LLCs are designed for simplicity and do not have to follow the same strict operational processes as S corporations. They have fewer formalities and do not require board meetings or annual shareholders‘ meetings.

However, effective management of an LLC still requires a range of skills, including organizational and technical expertise, to ensure smooth operations and business success.

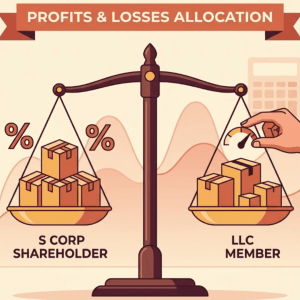

Additionally, LLC owners (members) have extensive flexibility in how they choose to manage their day-to-day operations. One significant area of flexibility is how they distribute profits and losses. Unlike S corporation shareholders who receive profits strictly based on their ownership percentage, LLC members can allocate profits and losses in a flexible manner.

Recent Comments