Alternative Lending: Fast Funding Solutions When Banks Aren't an Option

Navigate

In today’s dynamic business landscape, alternative lending has emerged as a lifeline for companies that need quick access to capital. While traditional banks have long dominated the lending industry, alternative lenders now offer viable pathways for businesses of all sizes to secure the funding they need. Whether you’re a startup seeking growth capital or an established company facing a cash flow gap, understanding your alternative lending options can make the difference between seizing an opportunity and watching it pass by.

This comprehensive guide explores everything you need to know about alternative lending, from how it works to the various financing options available in the market today.

What Is Alternative Lending?

Alternative lending refers to any financing solution that exists outside the conventional banking system. Unlike traditional lenders such as banks and credit unions, alternative lenders use innovative approaches to evaluate borrowers and provide funding faster than ever before.

The alternative lending industry has experienced explosive growth over the past decade. As traditional banks tightened their lending criteria following economic downturns, small businesses found themselves locked out of conventional financing. This gap in the market created opportunities for alternative lending platforms to step in and serve underserved borrowers.

Alternative business loans come in many forms, including:

Merchant cash advances

Invoice factoring

Peer to peer lending

Short term loans

Equipment financing

Business lines of credit

These alternative financing options cater to companies that may not qualify for traditional bank loans due to factors like credit history, time in business, or revenue requirements.

Why Businesses Choose Alternative Lenders Over Traditional Banks

Speed and Convenience

One of the most significant advantages of alternative lending is the speed of the application process. While traditional lenders often take weeks or even months to process business loans, many alternative lenders can provide funding within 24 to 48 hours. For businesses facing urgent cash flow needs, this fast funding capability is invaluable.

The application process with alternative lending platforms is typically streamlined and requires minimal paperwork. Borrowers can often complete applications online and submit financial documents digitally, eliminating the need for multiple in-person bank visits.

Flexible Credit Requirements

Traditional banks typically have strict minimum credit score requirements that exclude many small business owners from qualifying for loans. Alternative lenders take a more holistic approach to evaluating borrowers, considering factors beyond just credit score.

While having poor credit or bad credit can disqualify you from traditional loans, alternative business loans often remain accessible. Many alternative lenders focus on your business performance, cash flow, and revenue trends rather than solely relying on personal credit history.

Accessible to Small Businesses

Small businesses often struggle to meet the stringent requirements of traditional lenders. Banks typically prefer lending to established companies with extensive credit histories and substantial collateral. Alternative lending solutions bridge this gap by offering financing options designed specifically for small businesses and startups.

The alternative lending industry has democratized access to capital, allowing companies at various stages of growth to receive funding that was previously only available to larger corporations.

Types of Alternative Loans and Financing Options

Peer to Peer Lending

Peer-to-peer lending platforms connect borrowers directly with individual investors and institutional investors who have experience in funding loans. This alternative lending model bypasses traditional banks entirely, often resulting in competitive interest rates and more flexible terms.

Professional investors on these platforms evaluate loan requests and choose which businesses to fund. Borrowers benefit from a streamlined application process while investors earn returns on their capital.

Merchant Cash Advances

A Merchant cash advance provides businesses with upfront capital in exchange for a percentage of future credit card sales. This financing solution works well for retail businesses and restaurants with consistent card transactions. Borrowers pay back the advance automatically through their daily sales, making monthly payments predictable and manageable.

Unlike traditional fixed income allocations, merchant cash advances offer flexible repayment terms that adjust based on your sales volume. When business is slow, you pay less. When sales increase, repayment accelerates.

Invoice Factoring

Invoice factoring allows businesses to convert unpaid invoices into immediate working capital. Instead of waiting 30, 60, or 90 days for customers to pay, companies can sell their invoices to alternative lenders at a discount and receive funding quickly.

This alternative financing option is particularly valuable for B2B companies with reliable customers but lengthy payment terms. Invoice factoring provides fast cash without adding debt to your balance sheet.

Short Term Loans

Short term loans from alternative lenders provide quick access to capital with repayment terms typically ranging from three months to two years. These loans work well for businesses that need to cover temporary cash flow gaps, purchase inventory, or capitalize on time-sensitive opportunities.

While interest rates on short term loans may be higher than traditional bank loans, the speed and accessibility often justify the cost for borrowers who need fast funding.

Business Lines of Credit

Alternative lenders offer business lines of credit that function similarly to credit cards. Borrowers receive access to a predetermined credit limit and only pay interest on the amount they actually use. This flexibility makes lines of credit ideal for managing ongoing working capital needs.

Unlike traditional lenders that may require extensive collateral, many alternative lending platforms approve lines of credit based primarily on business performance and revenue.

Understanding Interest Rates and Repayment Terms

How Alternative Lenders Set Interest Rates

Interest rates from alternative lenders vary widely based on several factors:

Your credit score and credit history

Time in business

Annual revenue and cash flow

Industry risk factors

Loan amount and repayment terms

Because alternative lenders accept higher-risk borrowers than traditional banks, their interest rates often reflect this increased risk. Borrowers with poor credit or bad credit should expect to pay higher interest rates than those with strong credit profiles.

Comparing Costs Across Financing Options

When evaluating alternative loans, it’s essential to understand the true cost of borrowing. Some alternative lending options use factor rates rather than traditional interest rates, which can make direct comparisons challenging.

For illustrative purposes, consider these general ranges:

Traditional bank loans: 6% to 13% APR

Alternative business loans: 9% to 30% APR

Merchant cash advances: Factor rates of 1.1 to 1.3

Invoice factoring: 1% to 5% of invoice value

Understanding repayment terms is equally important. Some alternative lenders require daily or weekly payments, while others offer more traditional monthly payments. Plan ahead and ensure your cash flow can accommodate the payment schedule before committing to any financing solution.

How to Qualify for Alternative Business Loans

Minimum Requirements

While alternative lenders are more flexible than traditional banks, they still have basic requirements. Most reputable lenders look for:

Minimum time in business (typically 6 months to 2 years)

Minimum monthly or annual revenue

A minimum credit score (often lower than banks require)

Valid business bank account

Required financial documents

Preparing Your Application

To fast track the application process and improve your chances of approval, gather these financial documents before applying:

Business bank statements (3 to 6 months)

Tax returns

Profit and loss statements

Balance sheets

Business licenses and registrations

Having your paperwork organized demonstrates professionalism and helps lenders evaluate your business quickly.

Improving Your Approval Odds

Even with bad credit, you can take steps to strengthen your application:

Demonstrate strong cash flow and consistent revenue

Reduce existing debt where possible

Provide detailed explanations for any credit issues

Show a clear plan for how you’ll use the funds

Highlight positive business trends and growth potential

Choosing Reputable Lenders and Avoiding Predatory Practices

Identifying Trustworthy Alternative Lenders

The growth of the alternative lending industry has attracted both reputable lenders and predatory lenders. Due diligence is essential when evaluating funding options. Look for lenders who:

Clearly disclose all fees and interest rates

Have positive reviews from verified borrowers

Are members of industry associations

Provide transparent repayment terms

Offer responsive customer service

Red Flags to Watch For

Predatory lenders often target small business owners desperate for capital. Warning signs include:

Pressure to sign documents immediately

Unwillingness to provide written terms

Hidden fees or unclear pricing

Requests for upfront payments before funding

Interest rates that seem too good to be true

Financial institutions regulated by federal and state authorities offer more protection than unregulated lenders. Research any company thoroughly before sharing sensitive business information.

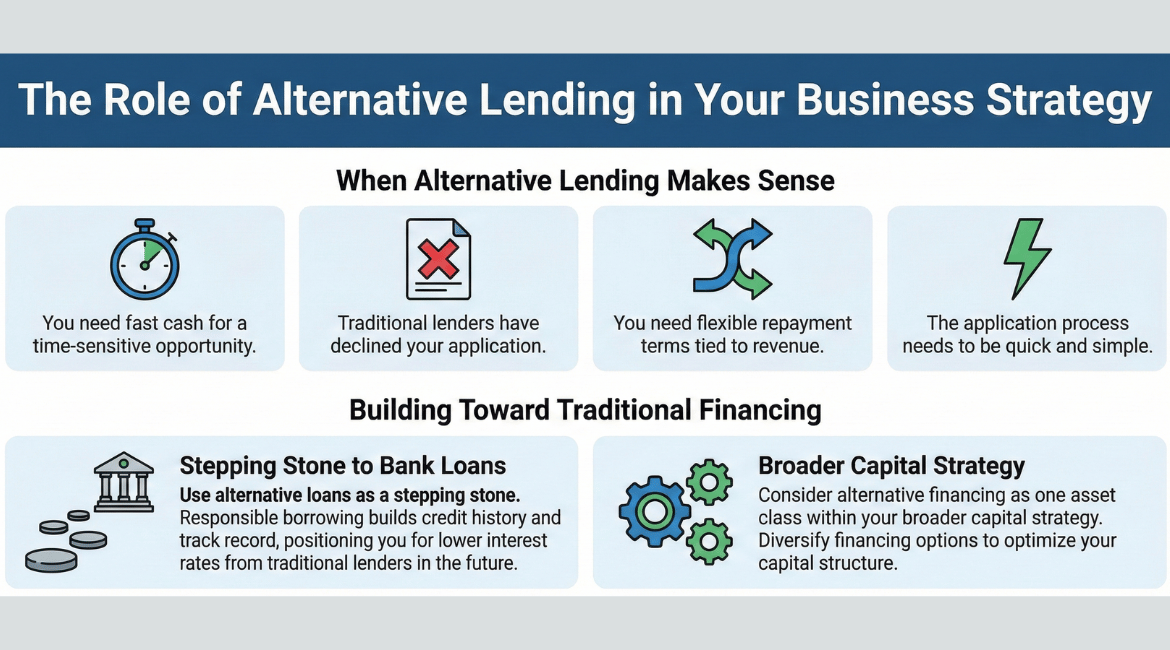

The Role of Alternative Lending in Your Business Strategy

When Alternative Lending Makes Sense

Alternative lending solutions work best in specific scenarios:

You need fast cash for a time-sensitive opportunity

Traditional lenders have declined your application

Your credit score doesn’t meet bank requirements

You need flexible repayment terms tied to revenue

The application process needs to be quick and simple

Building Toward Traditional Financing

Many small businesses use alternative loans as a stepping stone. By borrowing responsibly and making timely payments, you can build your credit history and business track record. This positions you to qualify for lower interest rates from traditional lenders in the future.

Consider alternative financing as one asset class within your broader capital strategy. Just as investors diversify their portfolios beyond traditional assets, smart business owners utilize multiple financing options to optimize their capital structure.

Investment Advice Disclaimer

This article is prepared solely for informational and illustrative purposes. Nothing contained herein constitutes investment advice or a recommendation regarding any particular security or financing option. The graphs provided and examples mentioned are for illustrative purposes only and do not guarantee future performance.

All information is current as of the date hereof and may change based on market conditions. Individual investors and business owners should conduct their own research and consult with financial professionals before making decisions. Such information should not be relied upon as the sole basis for any business or investment decisions.

Past performance is not indicative of future performance, and limited diversification in funding sources can increase business risk.

The Future of the Alternative Lending Industry

Technology and Innovation

The lending industry continues evolving rapidly. Alternative lending platforms leverage artificial intelligence, machine learning, and big data to evaluate borrowers more accurately than ever before. These technological advances allow lenders to assess creditworthiness beyond traditional metrics, opening doors for more borrowers.

As technology improves, expect the application process to become even faster and more seamless. Many companies now offer instant decisions and same-day funding for qualified borrowers.

Market Growth and Trends

The market for alternative lending continues expanding. More institutional investors are allocating capital to alternative lending platforms, increasing the funds available for business loans. This influx of capital benefits borrowers through more competitive interest rates and better terms.

Consumer loans through alternative lenders have also grown significantly, though this article focuses primarily on business financing. The principles of alternative lending apply across both markets, with speed, accessibility, and flexibility driving adoption.

Regulatory Developments

As the alternative lending industry matures, regulatory oversight is increasing. While some view regulation as a burden, reasonable oversight helps protect borrowers from predatory lenders and ensures fair lending practices.

Credit unions and traditional financial institutions are also entering the alternative lending space, blurring the lines between conventional and alternative financing options.

Conclusion: Is Alternative Lending Right for Your Business?

Alternative lending has transformed how small businesses access capital. By offering faster approval times, flexible credit requirements, and innovative financing solutions, alternative lenders fill a crucial gap left by traditional banks.

Whether you’re dealing with poor credit, need working capital quickly, or simply want to explore funding options beyond conventional loans, alternative lending deserves consideration. The key is understanding the various products available, comparing costs carefully, and choosing reputable lenders who operate transparently.

Remember to plan ahead when possible. While alternative lending provides fast funding when you need it, having time to compare options and negotiate terms typically results in better outcomes. Review all loan documents carefully, understand your repayment terms, and ensure the financing solution aligns with your business goals.

The alternative lending industry will continue growing and evolving. By staying informed about your options, you position your business to access the capital it needs whenever opportunities arise.

About Upwise Capital

Our team at Upwise Capital is here to assist you with every step of the way to secure whatever funding is needed to help your business grow. If you have any questions regarding how equipment financing works, please call our team at 77-55-UPWISE or email [email protected]. You can also apply online for alternative lending, so you can get back to work and running your business.

So…What do you think?

We want to hear from you. What do you think of this article, and was it helpful in your search for alternative lending?

Let us know by leaving a reply below. Feel free to share this article on your social media.

SHARE

Other Articles You May Want to Read

Recent Comments