Business Loans with Bad Credit: Your Complete Guide to Securing Financing Despite Credit

Navigate

Introduction

Starting or expanding a business when you have bad credit can feel like an uphill battle. Many entrepreneurs find themselves caught in a frustrating cycle: they need financing to grow their business, but traditional lenders require good credit scores that they simply don’t have. The good news? Business loans with bad credit are not only possible but increasingly accessible through various alternative lending options.

Whether you’re a startup founder with limited credit history or an established business owner who’s faced financial challenges, this comprehensive guide will show you exactly how to secure the business financing you need, regardless of your personal credit score.

Understanding Bad Credit and Business Loans

What Constitutes Bad Credit?

Before diving into loan options, it’s important to understand what lenders consider “bad credit.” Generally, a personal credit score below 580 is considered poor, while scores between 580-669 are deemed fair. However, when it comes to bad credit business loans, different lenders have varying definitions and minimum credit score requirements.

The Challenge of Traditional Business Financing

Traditional banks typically require excellent credit scores (usually 700+) for business loans, making it nearly impossible for entrepreneurs with poor credit to access conventional financing. This is where alternative lenders step in, offering small business loans specifically designed for borrowers with less-than-perfect credit histories.

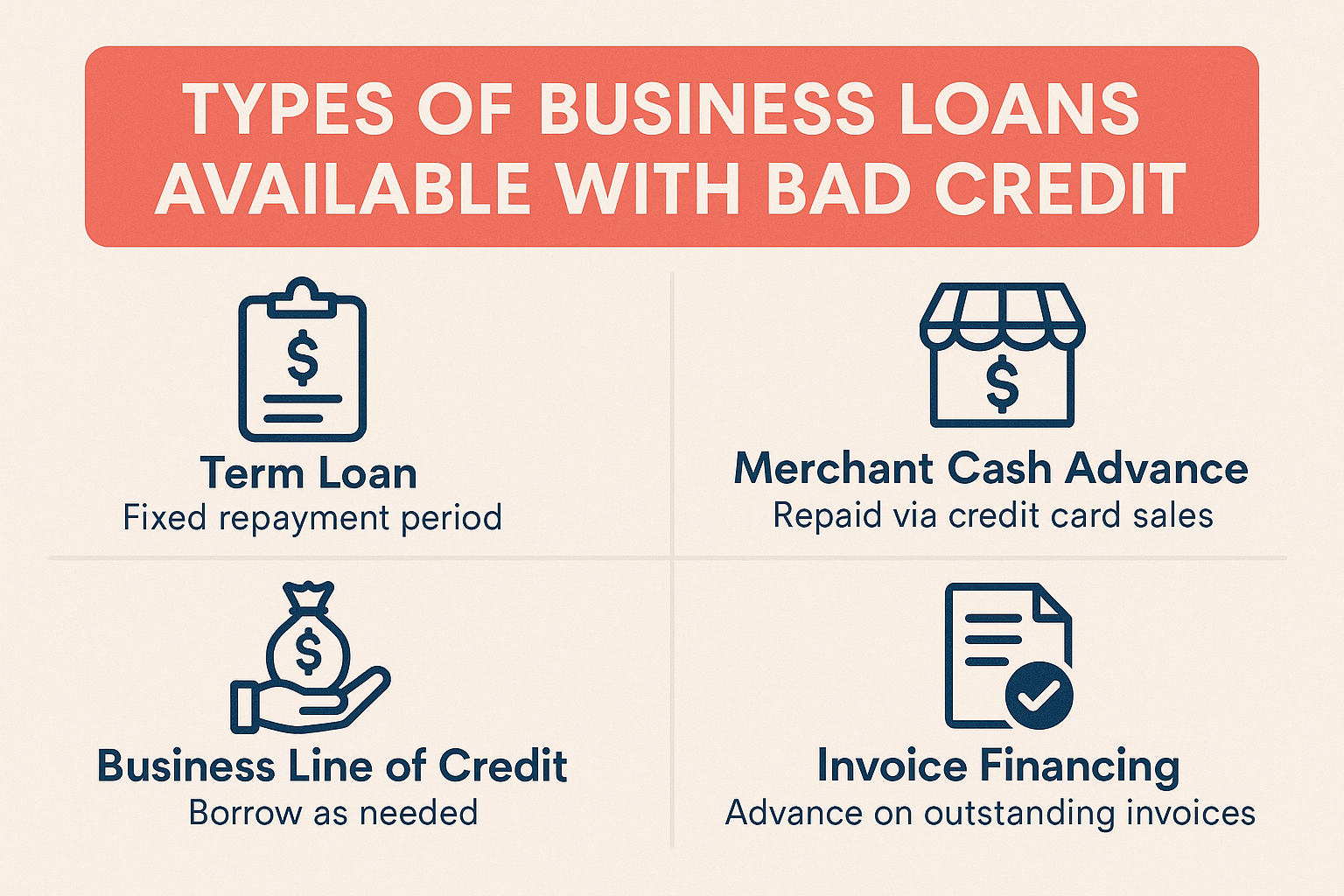

Types of Business Loans Available with Bad Credit

1. Merchant Cash Advances

Merchant cash advances are one of the most accessible forms of business financing for those with bad credit. Instead of focusing heavily on your credit score, these lenders primarily evaluate your business’s daily credit card sales and cash flow.

Key Features:

Quick approval process (often within 24-48 hours)

Minimal minimum credit score requirements

Repayment based on daily sales

2. Invoice Financing and Factoring

If your business has outstanding invoices from creditworthy customers, invoice financing or invoice factoring can provide immediate working capital without strict credit requirements.

Benefits:

Uses your invoices as collateral

Less emphasis on personal credit history

Improves cash flow quickly

Suitable for B2B businesses

3. Equipment Financing

Equipment financing is often easier to obtain with bad credit because the equipment itself serves as collateral. This reduces the lender’s risk and makes them more willing to work with bad credit borrowers.

4. Business Lines of Credit

A business line of credit provides flexible access to funds up to a predetermined limit. While traditional banks may be restrictive, many online lenders offer lines of credit to businesses with poor credit.

5. SBA Loans for Bad Credit

While SBA loans typically require good credit, some Small Business Administration programs are more flexible. The SBA’s microloans, for instance, may be available to borrowers with lower credit scores.

Alternative Lenders vs. Traditional Banks

Online Lenders

Online lenders have revolutionized business financing for entrepreneurs with bad credit. These platforms often use alternative underwriting methods that consider factors beyond just credit scores:

Annual revenue

Business bank account activity

Industry type and business model

Time in business

Credit Unions

Credit unions often have more flexible lending criteria than traditional banks and may offer better terms for small business owners with poor credit.

Peer-to-Peer Lending

P2P lending platforms connect businesses directly with individual investors, sometimes offering more personalized underwriting approaches.

Strategies to Improve Your Chances of Approval

1. Focus on Business Metrics

While your personal credit report may not be stellar, strong business fundamentals can compensate:

Consistent annual revenue

Positive cash flow trends

Strong business bank account history

Solid financial statements

2. Consider a Co-Signer or Personal Guarantee

Adding a co-signer with good credit or offering a personal guarantee can significantly improve your approval odds and potentially reduce interest rates.

3. Offer Collateral

Secured loans reduce lender risk. Consider offering personal assets or business assets as collateral to improve your chances.

4. Start Small

Begin with smaller loan amounts to establish a positive payment history, then gradually qualify for larger amounts.

What to Expect: Terms and Conditions

Interest Rates and Fees

Bad credit business loans typically come with higher interest rates than traditional financing. Rates can range from 10% to 99% APR, depending on:

Your credit score

Business performance

Loan type and amount

Repayment terms

Repayment Terms

Repayment terms vary widely:

Merchant cash advances: Daily or weekly payments

Working capital loans: 3-24 months typically

Equipment financing: 1-7 years

Business lines of credit: Revolving, pay as you use

Building Business Credit for the Future

Establish Business Credit History

While securing immediate financing is crucial, building business credit should be a long-term goal:

Open a business bank account

Apply for business credit cards

Work with suppliers who report to credit bureaus

Make all payments on time

Monitor Your Credit Reports

Regularly check both personal and business credit scores to identify areas for improvement and catch any errors.

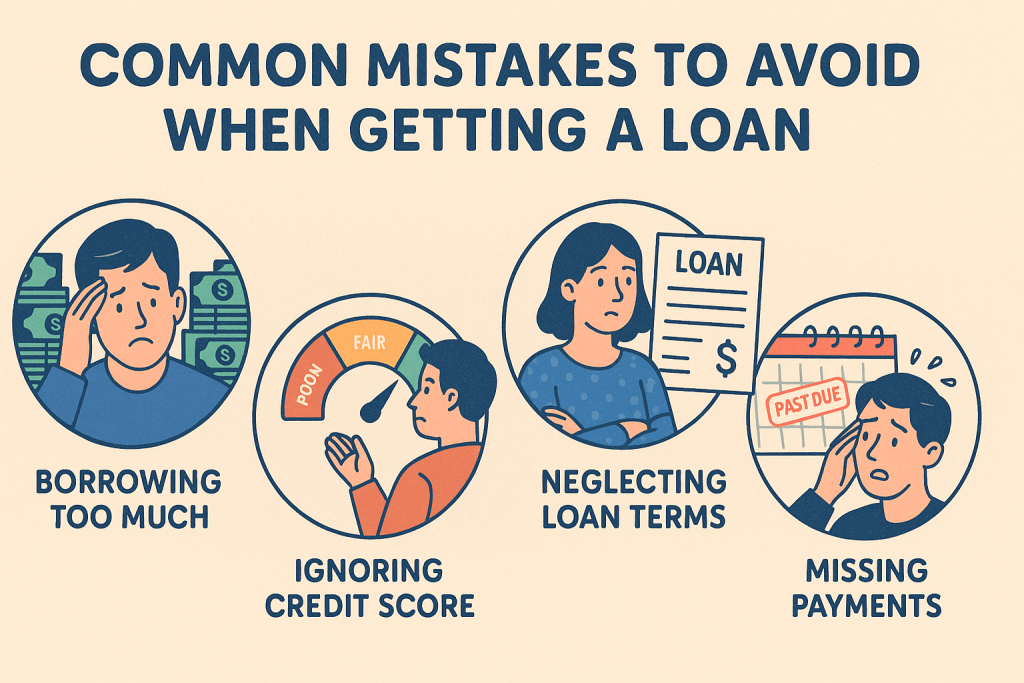

Common Mistakes to Avoid

1. Not Shopping Around

Different lenders have varying criteria. What one lender denies, another might approve.

2. Ignoring the Fine Print

Carefully review all terms, especially with merchant cash advances and other alternative financing options.

3. Borrowing More Than Necessary

Higher loan amounts mean higher risk and potentially worse terms.

4. Failing to Have a Repayment Plan

Ensure you can comfortably make payments without jeopardizing your business operations.

Alternatives to Traditional Loans

Business Credit Cards

Business credit cards can provide quick access to funds and may be easier to obtain than loans, even with bad credit.

Revenue-Based Financing

Some lenders offer financing based on your business’s revenue potential rather than credit history.

Crowdfunding

Consider crowdfunding platforms for specific projects or business expansions.

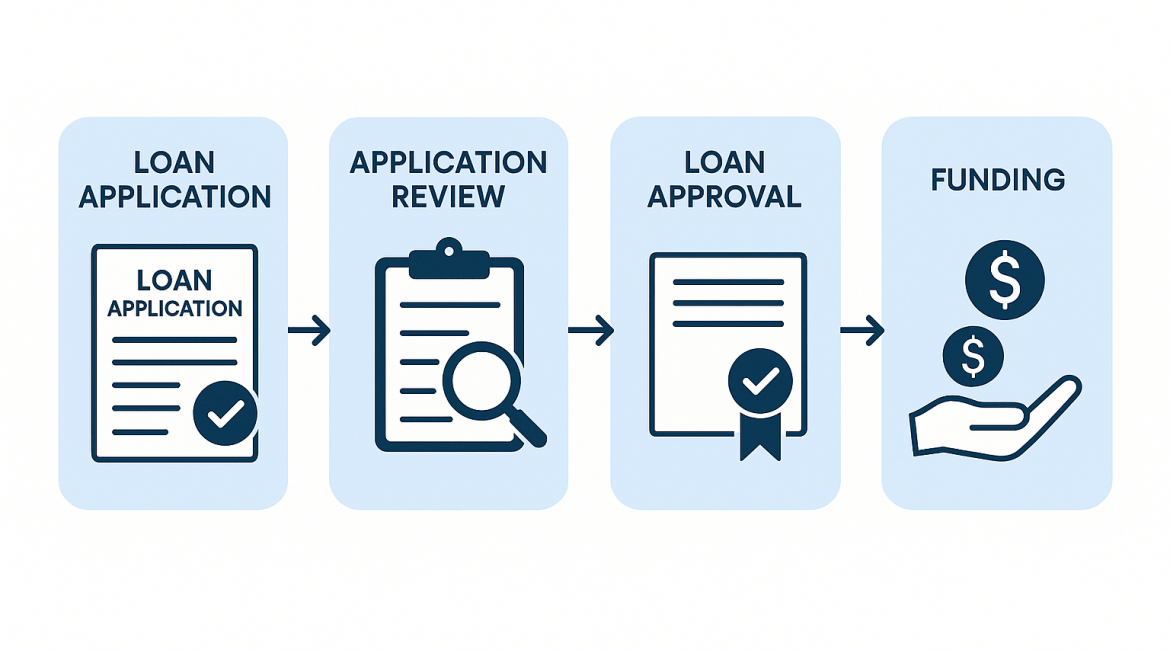

The Application Process

Required Documentation

Most lenders will require:

Financial statements

Business bank account statements

Tax returns

Credit report authorization

Business plan or use of funds statement

Timeline Expectations

Online lenders: 1-7 days

Traditional banks: 2-6 weeks

Merchant cash advances: 24-48 hours

SBA loans: 30-90 days

Future Outlook: Improving Your Credit

Short-Term Strategies

Pay all bills on time

Reduce debt to income ratio

Address any errors on your credit report

Keep credit utilization low

Long-Term Goals

Build relationships with lenders

Establish strong business credit

Gradually qualify for better terms

Eventually access traditional bank financing

Conclusion

Securing business loans may require more effort and research, but it’s entirely achievable. The key is understanding your options, preparing thoroughly, and selecting the most suitable type of financing for your specific business.

Remember that your current credit situation doesn’t define your business’s future. By making smart financing decisions today and focusing on building better credit over time, you’ll expand your access to better loan terms and more financing options as your business grows.

Ready to explore your options? Start by evaluating your business’s financial health, researching lenders that specialize in bad credit business financing, and preparing your application materials. Your business success story is waiting to be written. please call our team at 77-55-UPWISE or email [email protected]. You can also apply online for equipment financing, so you can get back to work and running your business.

SHARE

Other Articles You May Want to Read

Recent Comments