Business Debt Consolidation: The Complete Guide to Simplifying Your Company's Finances

Navigate

Managing multiple debts can quickly become overwhelming for any business owner. Between juggling various loan payments, keeping track of different interest rates, and maintaining healthy cash flow, it’s easy to see why so many entrepreneurs seek solutions to streamline their financial obligations. Business debt consolidation offers a strategic approach to combine multiple debts into a single, more manageable payment structure.

In this comprehensive guide, we’ll explore everything you need to know about business debt consolidation, including how it works, the benefits it provides, and how to determine if it’s the right choice for your company.

What Is Business Debt Consolidation?

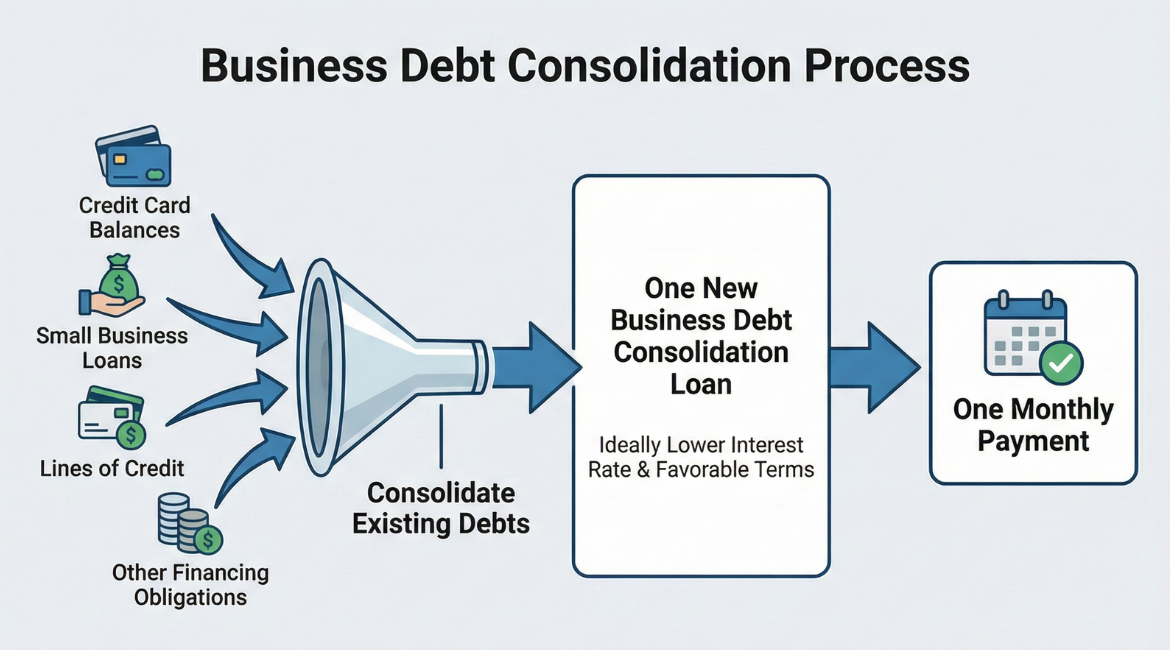

Business debt consolidation is the process of combining multiple business debts into one new loan with a single monthly payment. Instead of managing several payments to different lenders each month, you consolidate your existing debts into one consolidation loan that ideally comes with a lower interest rate and more favorable terms.

When you consolidate business debt, you’re essentially taking out a new business loan to pay off your existing loans, business credit cards, and other outstanding balance amounts. This leaves you with just one payment to manage, making it easier to budget and plan for your company’s financial future.

How Does a Business Debt Consolidation Loan Work?

The process of obtaining a business debt consolidation loan involves several key steps:

Assessment of Current Debts: First, you’ll need to determine exactly how much you owe across all your accounts. This includes credit card balances, small business loans, lines of credit, and any other financing obligations.

Loan Application: You’ll submit a loan application to a lender, providing details about your business, existing debts, and financial history. The lender will review your credit report and business credit score to assess your eligibility.

Approval and Funding: If approved, the lender provides funds to pay off your multiple loans and debts directly.

Repayment: You then make one monthly payment to the new lender according to the agreed-upon repayment terms.

Benefits of Business Debt Consolidation

There are numerous advantages to consolidating debt for your business. Understanding these benefits can help you determine whether this financial strategy aligns with your company’s goals.

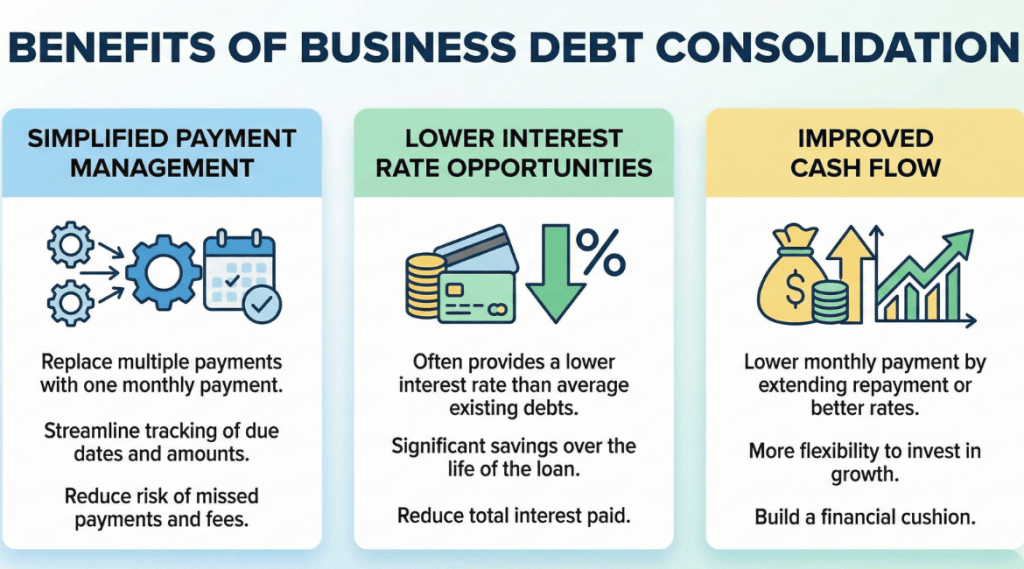

Simplified Payment Management

One of the most significant advantages of debt consolidation is the ability to replace multiple payments with one payment each month. Managing multiple types of debts means keeping track of various due dates, payment amounts, and interest rates. When you consolidate, you streamline this process considerably.

With a single payment structure, you reduce the risk of missed payments and the associated fees that come with them. This simplified approach allows you to focus more energy on growing your business rather than managing complex payment schedules.

Lower Interest Rate Opportunities

Many businesses accumulate high interest debt through business credit cards and short-term loans. A business consolidation loan often comes with a lower interest rate compared to the average rate across your existing debts. This can result in significant savings over the life of the loan.

By securing a lower interest rate, you reduce the total interest you’ll pay, which means more money stays in your business. Even a small reduction in interest rates can translate to substantial savings, especially for businesses with significant debt amounts.

Improved Cash Flow

Cash flow is the lifeblood of any business. When you’re making multiple payments to various lenders each month, it can strain your available funds and make it difficult to manage day-to-day operations.

A debt consolidation loan can provide a lower monthly payment by extending repayment periods or securing better rates. This improved cash flow gives you more flexibility to invest in growth opportunities, cover unexpected expenses, or build a financial cushion for your business.

Potential Credit Score Benefits

Constant on-time payments on your consolidation loan can positively impact your business credit score over time. Additionally, paying off credit card balances and other revolving credit can improve your credit utilization ratio, which is a factor in credit scoring.

A stronger credit score opens doors to better financing options in the future, including access to the most competitive rates when you need additional funding for business expansion.

Types of Business Debt Consolidation Loans

Several loan options exist for businesses looking to consolidate their debts. Understanding the different types available can help you choose the best solution for your specific situation.

Term Loans

Traditional term loans from banks, credit unions, or online lenders are among the most common options for debt consolidation. These loans provide a lump sum of funds that you repay over a set period with fixed interest rates and repayment terms.

Term loans typically offer competitive rates for businesses with strong credit and financial history. The predictable payment structure makes budgeting straightforward and helps you plan for long-term financial management.

SBA Loans

Small Business Administration (SBA) loans offer favorable terms and lower interest rates compared to many conventional loan products. While the loan application process can be more extensive, the benefits often make it worthwhile.

SBA loans are available through approved lenders and come with government backing, which reduces risk for lenders and allows them to offer better terms to borrowers. These loans work well for businesses that qualify and need substantial funds for consolidation.

Business Lines of Credit

A business line of credit provides flexible access to funds that you can use to pay off existing debts. Unlike a traditional loan where you receive a lump sum, a line of credit allows you to draw funds as needed up to your approved limit.

This option works well for businesses that want flexibility in how they consolidate and pay down their debts. You only pay interest on the amount you actually use, which can save money if you’re strategic about your consolidation approach.

Alternative Lending Options

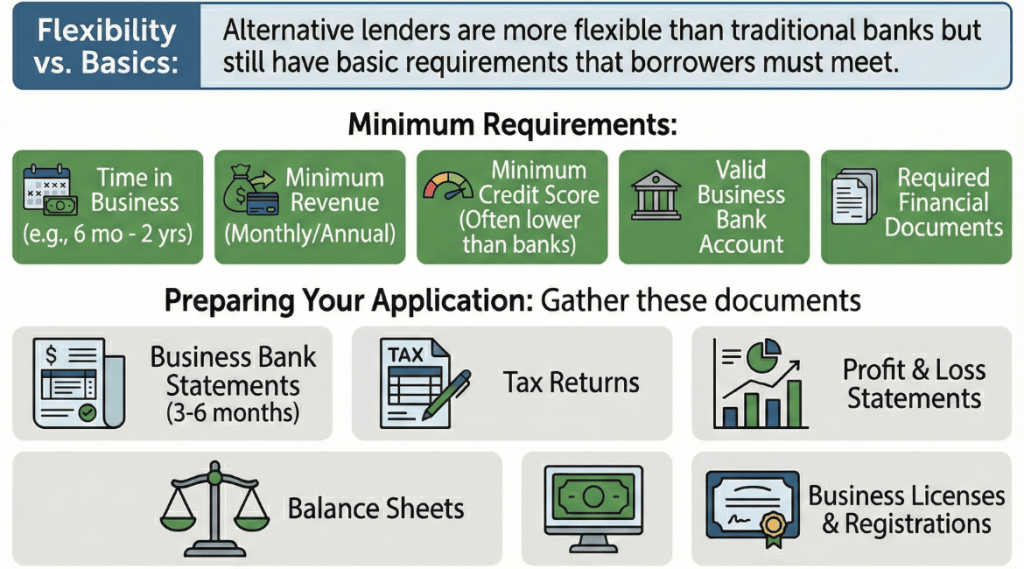

Alternative lenders and online lenders have expanded options for businesses that may not qualify for traditional financing. These lenders often have more flexible eligibility criteria and faster approval processes.

While interest rates from alternative lenders may be higher than traditional banks, they provide access to funds for businesses with less established credit histories or those needing quick access to financing.

How to Qualify for a Business Debt Consolidation Loan

Understanding the eligibility criteria for consolidation loans helps you prepare a strong application and improve your chances of approval.

Credit Requirements

Lenders will examine both your personal and business credit when evaluating your loan application. A higher credit score typically results in better rates and terms. Before applying, review your credit report to understand where you stand and address any errors that might negatively impact your score.

If your credit needs improvement, consider taking steps to strengthen it before applying. This might include paying down personal credit cards, ensuring all payments are current, and correcting any inaccuracies on your credit report.

Business Financial Health

Underwriters want to see that your business generates sufficient revenue to cover the new loan payment. They’ll typically request financial statements, tax returns, and bank statements to assess your company’s financial health.

Strong cash flow and consistent revenue demonstrate your ability to manage repayment and reduce lender risk. Prepare these documents in advance to streamline the application process.

Time in Business

Many lenders prefer to work with established businesses that have been operating for at least 1-2 years. This track record provides evidence of stability and reduces perceived risk.

However, newer businesses still have options through alternative lenders who specialize in working with companies at various stages of development.

Collateral Considerations

Some consolidation loan options require collateral to secure the financing. Collateral can include business assets, equipment, real estate, or other valuable property.

Secured loans often come with lower interest rates because the collateral reduces lender risk. However, it’s important to understand that you risk losing the pledged assets if you fail to meet repayment obligations.

Costs and Fees to Consider

While debt consolidation can save money in many cases, it’s essential to understand all associated fees and costs before proceeding.

Origination Fee

Many lenders charge an origination fee to process your loan. This fee typically ranges from 1% to 5% of the loan amount and is either deducted from your funds or added to the loan balance.

Factor this cost into your calculations when determining whether consolidation makes financial sense for your business.

Prepayment Penalties

Some loans include prepayment penalties if you pay off the balance before the end of the loan terms. If you anticipate being able to pay off your debt early, look for consolidation options without these penalties.

Interest Costs Over Time

While a lower monthly payment is attractive, be aware that extending repayment periods can result in paying more total interest over the life of the loan. Calculate the total cost of the consolidation loan compared to what you would pay by continuing with your current debt structure.

Application and Processing Fees

Some lenders charge fees for processing your loan application or for other administrative costs. Ask about all potential fees upfront so you can accurately compare options and determine the true cost of consolidation.

When Business Debt Consolidation Makes Sense

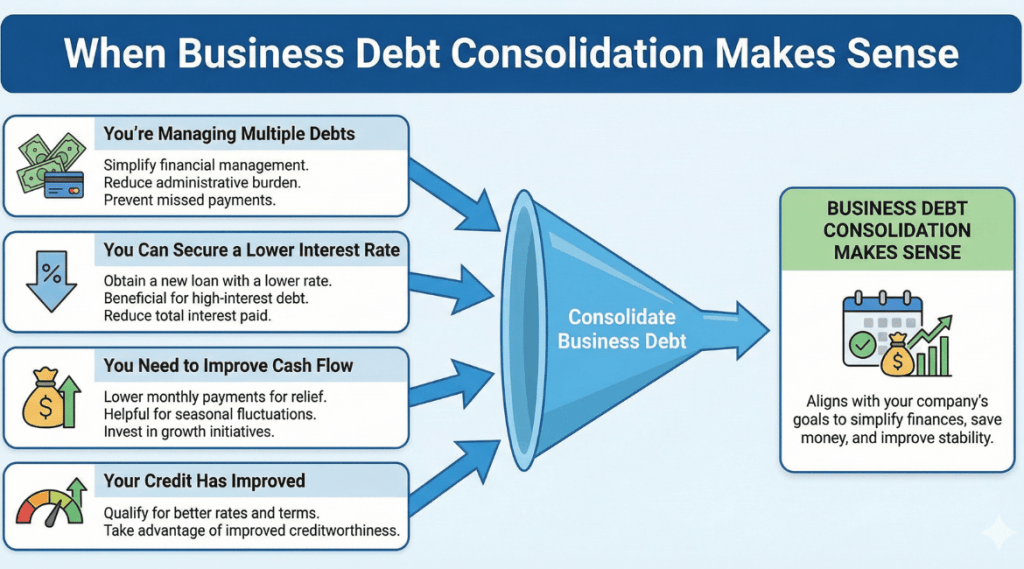

Consolidating debt isn’t the right choice for every business situation. Here are scenarios where it typically makes the most sense:

You're Managing Multiple Debts

If you’re currently handling multiple payments to different lenders each month, consolidation can significantly simplify your financial management. The convenience of one payment instead of many reduces administrative burden and helps prevent missed payments.

You Can Secure a Lower Interest Rate

Consolidation is most beneficial when you can obtain a new loan with a lower interest rate than what you’re currently paying. This is especially true if you have high interest debt from credit card balances or short-term loans.

You Need to Improve Cash Flow

If your current payment obligations are straining your cash flow, a consolidation loan with lower payments can provide relief. This is particularly valuable for businesses experiencing seasonal fluctuations or those investing in growth initiatives.

Your Credit Has Improved

If your credit has improved since you took out your existing loans, you may now qualify for better rates and terms. Consolidating allows you to take advantage of your improved creditworthiness.

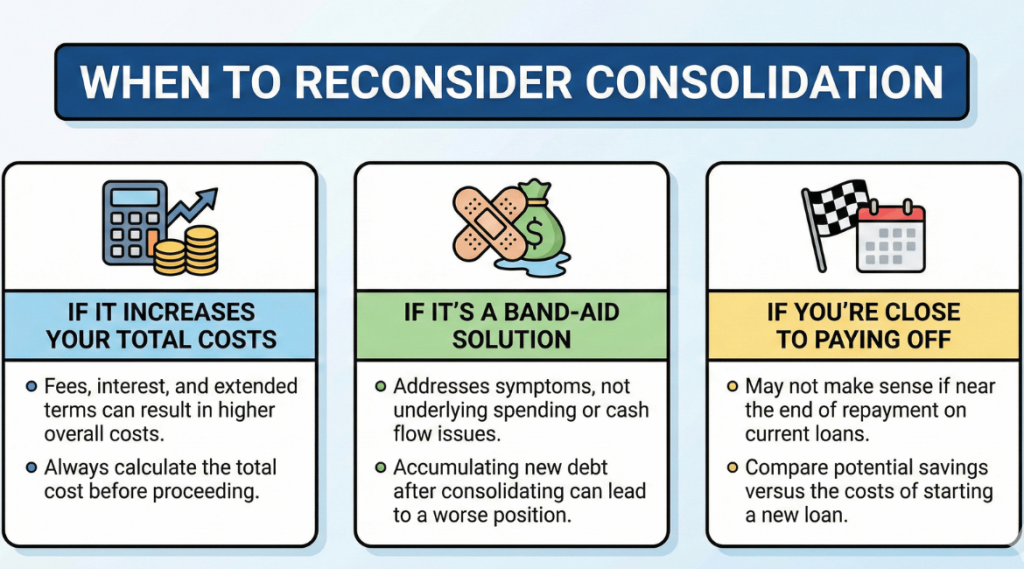

When to Reconsider Consolidation

There are also situations where consolidation may not be the best strategy:

If It Increases Your Total Costs

Sometimes the fees, interest, and extended repayment terms of a consolidation loan result in higher overall costs than sticking with your existing debts. Always calculate the total cost before proceeding.

If It's a Band-Aid Solution

Consolidation addresses the symptoms of debt but doesn’t fix underlying issues with spending or cash flow management. If your business continues to accumulate new debts after consolidating, you’ll end up in a worse position than before.

If You're Close to Paying Off Existing Debts

If you’re near the end of repayment on your current loans, it may not make sense to start over with a new loan. Calculate how much you’d save versus the costs of starting fresh.

Steps to Consolidate Your Business Debt

Ready to move forward with consolidation? Follow these steps to manage the process effectively.

Step 1: Assess Your Current Debt Situation

Start by creating a comprehensive list of all your existing debts. Include the lender, outstanding balance, interest rate, monthly payment, and remaining repayment terms for each debt. This gives you a clear picture of what you need to consolidate.

Step 2: Determine Your Goals

What do you hope to achieve through consolidation? Whether it’s to save money on interest, lower payments, or simplify your finances, having clear goals helps you evaluate whether specific consolidation options meet your needs.

Step 3: Research Lenders

Explore options from various sources, including traditional banks, credit unions, online lenders, and alternative lenders. Compare interest rates, fees, repayment terms, and eligibility criteria across multiple types of lenders.

Consider working with a loan officer who can provide guidance and help you understand your options. They can answer questions and assist with the application process.

Step 4: Prepare Your Application

Gather all necessary documentation, including financial statements, tax returns, bank statements, and information about your existing loans. A complete application speeds up the approval process.

Step 5: Compare Offers and Choose Wisely

If you receive multiple offers, compare them carefully. Look beyond just the interest rate to consider total costs, fees, repayment periods, and any restrictions or penalties.

Step 6: Pay Off Existing Debts

Once approved, use the funds from your new loan to pay off all your existing debts. Confirm that each account shows a zero balance and request confirmation from each lender.

Step 7: Manage Your New Loan Responsibly

Set up automatic payments to ensure you never miss a due date. Continue monitoring your finances and avoid accumulating new debts that could put you back in a difficult situation.

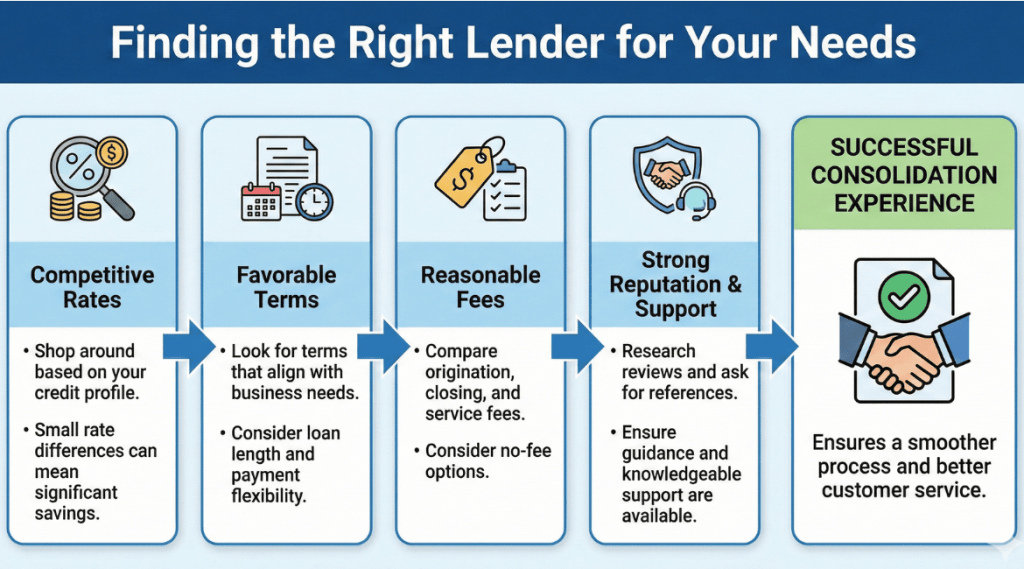

Finding the Right Lender for Your Needs

Choosing the right lender is crucial for a successful consolidation experience. Here’s what to look for:

Competitive Rates

Shop around for the most competitive rates available based on your credit profile and business qualifications. Even small differences in rates can translate to significant savings over time.

Favorable Terms

Look for lenders offering repayment terms that align with your business needs. This includes the loan length, payment flexibility, and any options for temporarily lower payments during slow periods.

Reasonable Fees

Compare all associated fees, including origination fees, closing costs, and any ongoing service charges. Some lenders offer no-fee options that may be worth considering.

Strong Reputation

Research lender reviews and ask for references from other business owners. Working with a reputable lender ensures a smoother process and better customer service if issues arise.

Assistance and Support

Consider whether the lender offers guidance and assistance throughout the process. Having access to knowledgeable support can make the experience less stressful and help you make informed decisions.

Alternatives to Traditional Debt Consolidation

If a traditional business debt consolidation loan isn’t the right fit, consider these alternatives:

Debt Management Plans

Working with a credit counseling service can help you negotiate better terms with existing creditors without taking out a new loan. This approach can lower interest rates and create more manageable payment structures.

Balance Transfer Options

For debts primarily on business credit cards, a balance transfer to a card with a promotional low rate can provide temporary relief and savings on interest.

Renegotiating Existing Terms

Sometimes lenders are willing to renegotiate loan terms directly, especially if you’re experiencing financial difficulties. This might include extending repayment periods or adjusting interest rates.

Invoice Financing

If cash flow is your primary concern, invoice financing allows you to access funds tied up in unpaid invoices. This can provide the money needed to pay down debts without taking on additional long-term financing.

Maintaining Financial Health After Consolidation

Successfully consolidating your debts is just the first step. Maintaining financial health requires ongoing attention and discipline.

Create a Budget

Develop a comprehensive budget that accounts for your new consolidation payment and all other business expenses. Stick to this budget to avoid accumulating new debts.

Build an Emergency Fund

Set aside funds for unexpected expenses so you don’t have to rely on credit when challenges arise. Even small regular contributions to savings can build a meaningful cushion over time.

Monitor Your Credit

Regularly check your credit report and scores to track your progress and catch any issues early. Improving your credit opens doors to better financing options for future business needs.

Avoid New Debt Accumulation

Be cautious about taking on new debts while repaying your consolidation loan. If additional financing is necessary, carefully evaluate whether it’s essential and how it fits into your overall financial plan.

Conclusion

Business debt consolidation can be a powerful tool for simplifying your finances, reducing interest costs, and improving cash flow. By combining multiple debts into a single loan with better terms, you can focus more on growing your business and less on managing complex payment schedules.

However, consolidation isn’t right for every situation. Carefully evaluate your current debts, research your options, and calculate the total costs before making a decision. With the right approach, a business debt consolidation loan can help you regain control of your finances and position your company for long-term success.

Take the time to determine whether consolidation aligns with your business goals, qualify for the best rates possible, and manage your new loan responsibly. With these strategies in place, you’ll be well on your way to a healthier financial future for your business.

Our team at Upwise Capital is here to assist you with every step of the way to secure whatever funding is needed to help your business grow. If you have any questions regarding how equipment financing works, please call our team at 77-55-UPWISE or email [email protected]. You can also apply online for equipment financing, so you can get back to work and running your business.

So…What do you think?

We want to hear from you. What do you think of this article and was it helpful in your search for equipment financing?

Let us know by leaving a reply below. Feel free to share this article on your social media.

SHARE

Other Articles You May Want to Read

Recent Comments