Cannabis Construction Financing For Your Facility

Navigate

When it comes to running and operating a successful cannabis business, being able to build out a successful and profitable facility is a big piece of the puzzle. Knowing the right layout, how to maximize your square footage, the type of cannabis equipment you should purchase, how to create the most energy-efficient facility, and finding the right partners and best capital sources can be a daunting task. Make sure that whatever you do, surround yourself with people who have been in the cannabis industry for years and have already made their mistakes with the construction and building of a cannabis facility whether it is cultivation, manufacturing, distribution, lab, or retail property.

Choose Your Partners Wisely

Upwise Capital is very bullish on the cannabis space with over $150MM in construction financing transactions closed helping to build out cannabis facilities throughout the United States in legal cannabis markets. I have been funding cannabis companies since early 2014 and have years of experience raising debt capital for cannabis companies with a specialty in building out cannabis cultivation and manufacturing facilities. When it comes to cannabis construction financing, most lenders will require a 1st lien position on the property and they will help with the build-out and CAPEX needed to get the facility operational or producing.

We focus on underserved areas of the cannabis industry:

New Construction (From the Ground Up)

Projects with build-out, Rehab, Remodels, and Tenant Improvements with a value-add component

Acquisitions and Refinances

Requests that require higher leverage (case by case)

TI’s, Equipment Financing, and FF&E

Landlord refinancing for bank loans that have been called due to a cannabis tenant

Cannabis Values

What separates Upwise from most lenders is that we consider true cannabis valuations when underwriting the transactions we take on as opposed to traditional non-cannabis values that most other lenders use as a basis. This enables our borrowers to secure significantly higher leverage on both stabilized properties and value-add projects. The ability to lend on the cannabis value of a property in limited license states allows us to complete a full project from beginning to end, rather than in phases. Typically for stabilized property, the lender will offer a higher loan to value and the cost of capital and terms will be better. On stabilized assets, lenders will typically lend 65% LTV to 80% LTV based on the as-completed cannabis value or as is real estate value. For start-up facility build-outs or value add tenant improvements and FF&E, cannabis lenders will typically lend 50% LTV to 60% LTV based on the as-completed cannabis real estate value of the property. Most marijuana construction loans will require full recourse. Non-recourse cannabis business loans are available to publicly traded companies or cannabis-related businesses that have a lot of investors on the cap table.

What are your options for cannabis facility construction loans?

Facilities

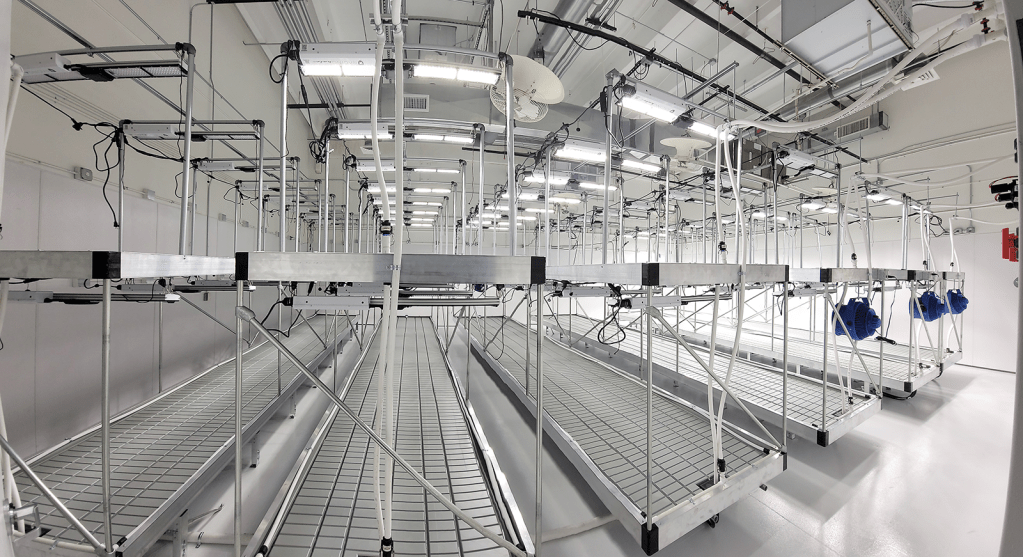

Cultivation Facility — Many lenders are surfacing for the build-out, construction, and equipment needed within a cannabis growing facility. If the lender has experience in the cannabis facility industry, they will understand and lend against the as completed cannabis value. Loans can be used for acquisitions of property, tenant improvements, ground-up construction, CAPEX or equipment, rehabs, and refinances typically requiring a first lien mortgage position on the property.

Manufacturing Facility — Many lenders are surfacing for the build-out, construction, and equipment needed within a cannabis manufacturing facility. If the lender has been in the industry for many years they will understand and lend against cannabis value. Loans can be used for acquisitions of property, tenant improvements, ground-up construction, CAPEX or equipment, rehabs, and refinances typically requiring a first lien mortgage position on the property.

Dispensaries

Recreational Dispensary — Most traditional commercial real estate lenders are reluctant to fully embrace the retail dispensary business model, even though dispensaries were pandemic proof like liquor stores. Public and private REITS, sale-leaseback firms, private debt institutions, and private equity financing are available to medical or recreational dispensaries. Lenders are ideally looking for limited license states and prime locations when accessing a retail store.

Medical Dispensary — Most cannabis real estate lenders are reluctant to fully embrace the dispensary business model, even though retail dispensaries were pandemic proof like liquor stores. Public and private REITS, sale-leaseback firms, private debt institutions, and private equity financing are available to medical or recreational dispensaries. Lenders are ideally looking for limited license states and prime locations when accessing a retail store.

Processing

Lab Financing – Many lenders are surfacing for the build-out, construction, and equipment needed within a cannabis manufacturing facility. If the lender has been in the industry for many years they will understand and lend against cannabis value. Cannabis real estate loans can be used for acquisitions of commercial property, tenant improvements, ground-up construction, CAPEX or equipment, rehabs, and refinances typically requiring a first lien mortgage position on the property.

Other

Equipment Loans and Leasing — If you need capital to buy new equipment or leverage existing unencumbered equipment, loans, and leasing options are available for acquiring and upgrading various equipment used in the cannabis manufacturing process. Equipment that is already owned can be leveraged through a sale-leaseback. Some equipment that can be financed includes growing and processing equipment, including lighting, HVAC, Racking, extraction equipment, energy systems, kitchen equipment, and other cannabis equipment. Upwise works with some of the best cannabis equipment manufacturers in the country such as Fluence lighting, Fohse LED, Sync Lighting, PIPP Horticulture, Glow Glide, Quest HVAC, Hawthorne Gardening Center, Grow Generation, and more.

Cannabis Business Loans or Term Loans— Some term loans are available to stabilized cannabis operators who are showing a net profit and have a proven track record. Most business loans in the cannabis industry are from private institutions that are looking for secured returns from their loan products. Most lenders require real estate, licenses, or equipment as collateral with a blanket lien across all business assets. Some banks are lending to cannabis companies that are publicly traded or MSOs, operating in multiple states at a profit.

Cannabis Bank Loans – These cannabis loans are available for profitable cannabis operators through almost 35 + banks and small credit unions throughout the united states. A lot of these banks that are lending to cannabis businesses require the CRB to bank with the institution as well. Interest rates are low for cannabis bank loans, typically 5% – 8% over 5 to 15-year terms with a 25-year amortization schedule. These loans are senior secured will a blanket lien on all business assets including real estate. For real estate secured bank loans, the banks are lending at 50% to 60% loan to value based on the liquidation value of the real estate asset appraised by an MAI certified appraisal firm.

Tenancy Requirements for Cannabis Owner-Occupants

1. Real estate ownership is organized as a special purpose entity (Ownership SPE), which sole purpose/business is the ownership and operation of the subject real estate property.

2. The same principles of this Ownership SPE, create another SPE to operate as the tenant (Tenant SPE). The purpose of this separate Tenant SPE is the operation of the cannabis business –growing – harvesting – processing – distribution – retail – including everything that is involved with running this cannabis business. This Tenant SPE does not own the real estate.

3. The Ownership SPE then enters into a lease with the Tenant SPE, at market rents, NNN, for a term of 10 to 50 years.

4. The reason: If this Tenant SPE fails, for whatever reason, the property is still owned by the Ownership SPE, and ready to be leased to any other tenant. The undisturbed mortgage remains in place. The SPE also acts as the non-cannabis entity allowing for other tax deductions

5. Market rent is what similar cannabis-producing, processing, distribution, and retailing tenants are paying elsewhere in the region, where the real estate is located. Market rent is defined by the appraisal.

6. Value of the real estate is therefore based on a reconciliation of:

a. Discounted Cash-Flow, or Income method, based on the Net Operating Income (NOI) received as a result of the tenant’s rents.

b. Market sales of comparable properties with comparable tenancies in that region.

7. “Going Concern” value does NOT apply for a cannabis transaction as that’s only for a hotel! However, the use of cannabis valuation is taken into account in these cannabis appraisals.

8. Replacement value, or the total value of improvements made, does not count at all towards as-is value. Any capital improvements made to the property will be taken into account.

9. The equipment, furnishings, special machinery, inventory, receivables, vehicles, and supplies, do not factor into the real estate loan transaction at all. They are not used as collateral either, so these assets can be leveraged with other financings. This makes no impact on the real estate transaction, the property value, etc.

10. If the property is seasoned for at least 18 months, a cash-out refinance is possible.

11. For a seasoned stabilized cannabis property (12 to 18 months), we can offer longer-term options between 5 to 25-year terms depending on the structure.

12. For a startup, where we are prepared to make a construction or major renovation loans and any equipment or CAPEX requirements including up to 100% LTV on cannabis-specific equipment

13. Any first mortgage, real estate taxes, or liens that are owed will be paid in full at closing.

14. For Cannabis Real Estate Sale-Leaseback transactions we can provide solutions to indoor facilities, greenhouse operations, processing facilities, outdoor grow operations, and dispensaries.

Our team at Upwise Capital is here to assist you with every step of the way to secure whatever funding is needed to help your business grow. If you have any questions regarding how cannabis facility financing works, please call our team at 77-55-UPWISE or email [email protected]. You can also apply online for construction financing, so you can get back to work and running your business.

So…What do you think?

We want to hear from you. What do you think of this article and was it helpful in your search for construction financing?

Let us know by leaving a reply below. Feel free to share this article on your social media.

Apply for a Cannabis Construction Loan Today.

- Pursue new opportunities, upgrade operations, support inventory or boost marketing efforts.

- Apply today to unlock working capital that supports your goals without restrictions.

- Close the cash flow gap within your cannabis company or bridge the financing divide between your short-term and long-term goals.

Stay ahead of the curve - get access today!

SHARE

Recent Comments

| Rahul Gupta on Business Loan with Bank Statem… | |

| Joe on How Cannabis MCA Funding Can H… | |

| John on Opening a dispensary? See how… | |

| Toluwalope Oyeleye on Advantages and Disadvantages o… | |

| Knote on The Ultimate Guide to Short Te… |

Other Articles You May Want to Read

2 Comments

Wondering if you are providing or considering providing commercial real estate loans for psilocybin service centers in Oregon. We are seeking to buy a building to operate a service center that will begin operations in 2023. Any thoughts?

Yes we definitely can. Give us a call or send an email to [email protected] so we can discuss further